The balance sheet is one of the 3 most important financial statement used to evaluate a business. It provides information about 3 general items of the company:

- Assets: what the company owns.

- Liabilities: what the company owes.

- Equities: what is the investment done by shareholders in the company.

1. Information disposal #

The balance sheet consist of different hierarchies of items which in the end represent a variety of G/L accounts. All these items and accounts are disposed in 2 sides and each side should sum the same amount (Assets = Liabilities + Shareholder’s Equitiy). That’s the reason why it’s called balance sheet.

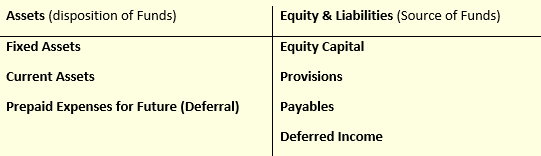

Here you can see some usual items at a very high level in a balance sheet:

The items and accounts disposal can be adjusted according to the company needs using an specific FI Statement Version.

1.1 Debit side – Assets #

In the debit side you find the assets, which are the result of the disposition of funds.

1.1.1 Fixed assets

These are long-term or fixed asset items:

- Intangible.

Intangible assets are those that have a value despite not being physical. Here are some examples: patents, intellectual property, and brand name.

- Tangible assets.

Tangible assets could be buildings, machinery and equipment, vehicles, fixture and fittings, low-value assets, assets under construction.

- Financial.

Financial assets are long-term investments and secuirities.

1.1.2 Current assets

These are current asset items:

- Inventory.

The inventory consist of the goods the company has available for sale.

- Accounts receivable.

This asset represent the money that hasn’t been paid yet by the clients.

- Securities, stocks, bonds.

These are financial investments that can be converted to cash in the short term.

- Cash and cash equivalents.

These assets represent cash, short-term deposits, or short-term country debt obligation.

1.1.3 Prepaid expenses

Prepaid expenses are expense deferrals, which involves a payment in advance to cover several periods. The portion of the amount paid that corresponds to future periods should be reported as a current asset and not as an expense. A common example is the payment of an insurance premium.

1.2 Credit side – Equity & Liabilities #

In the credit side you find the equity and liabilities, which are the source of funds.

1.2.1 Shareholder’s equity / Equity Capital

These are equity capital items:

- Capital stock.

It’s the amount of equity or shares that a company has and is authorized to sell.

- Capital reserve.

It’s the money created out of capital profit which is kept aside to finance long-term future projects or to write-off future capital losses in crisis periods.

- Revenue reserve.

It’s the revenue that a company keeps aside in a special account for future needs or for a specific purpose, such as covering potential losses.

- Retained earnings.

It’s the revenue kept by the company rather than being distributed as dividends to shareholders.

- Net Proft/Net loss of the year.

If a company has net profit, you’ll see it here. The net profit is all the revenue minus expenses.

1.2.2 Liabilities

A company liability is the money that the company owes to another party.

1.2.2.1 Liabilities – Provisions

Provisions are funds set aside to cover specific future expenses. These could be provisions for:

- Pensions.

- Taxtation.

- Other subjects.

1.2.2.2 Liabilities – Payables

The following items are current payables:

- Liabilities to banks.

This payable represents the money you pay to banks, usually because of loans or bank comissions.

- Deposits received.

This payable represents the money paid in advance by customers. If the service or good compromised is not provided the company will have to pay back a refund.

The following items are long-term payables:

- Accounts payable.

Accounts payables or trade payables represent the debt you acquire when you receive the invoices from vendors or suppliers.

- Wages or salaries.

1.2.2.3 Liabilities – Deferred Income

Deferred income or revenue deferral means that the company has already received the money for a service whose invoice has been issued, although the service last several months. This is usually the case of insurance premiums, and each month the company has to report the unearned amount as a current liability.

2. Run the balance sheet #

In the next example you’ll see how to run the Balance Sheet and compare values with the previous year to check which is the trend in a specific item:

3. How to use the balance sheet #

The balance sheet is used to calculate different ratios that analysts assess in order to gain insight into the business financial status.

The balance sheet provides a snapshot of the company at a partitcular moment. In order to see trends, you should compare the figures with those of the previous periods, or with the same period of previous year.

With the balance sheet the company can assess:

- Whether the borrowed money is too much.

- Which part of the assets are liquid assets (those considered cash or that can be quickly converted to cash).

- Whether there is enough cash to meet payment needs.

4. Related topics #

The following topics have been mentioned in this topic and you should consider going over them:

5. Related transactions and apps #

Related Fiori apps:

- Maintain FI Statement Verions (like OB58).

- alance Sheet/Income Statement.

Related transactions:

OB58

Maintain FI Statement versions (create, copy, change, delete).

S_ALR_87012284

Financial Statement Report (RFBILA00 program). It displays all hierarchy and items. You can choose different output options (classical list, ALV grid or tree).