The bank reconciliation is the analysis and matching of all transactions recorded by the company (in the cashbook) with all those recerived by the bank (in the passbook or bank statement).

Every company must have at least one bank account. The balance of that account is provided by the bank and it changes with each transaction. Every day the bank account has an openning balance, and also an ending balance, once the day is over and all its transactions have been posted. Large companies could have thousands of transactions every day, and posting all of them manually is not possible.

To automate that process, companies will use the Electronic Bank Statement (EBS). When all items can be posted automatically, the G/L account that represents the passbook will have the same balance as the bank statement.

The main aim of the bank reconciliation is to have that same balance, ensuring that the cashbook has also been posted by the right transactions. Differences may arise, and they should be analyzed to find the reason and proper solution.

1. Reasons of the balance difference #

The difference between the cashbook balance and the passbook is usually due to the lack of some postings (credits received or charges made) that the department has not recorded yet into the system.

It can also be because some checks issued have not been sent to the bank. Additionally, sometimes the difference is due to mistakes commited by the company or even the bank.

2. Approach #

In order to make possible the reconciliation process, the company should not use the G/L bank account in its business transactions. Other G/L accounts should be used instead. They are called bank clearing accounts, and there is usually one per payment method. They represent the cashbook.

When the bank statement (passbook) is received, it usually contains many items that are posted into the system using the G/L bank account. When an item represents a payment:

- It should also post the corresponding bank clearing account.

- It is considered as the confirmation of the payment in the bank account.

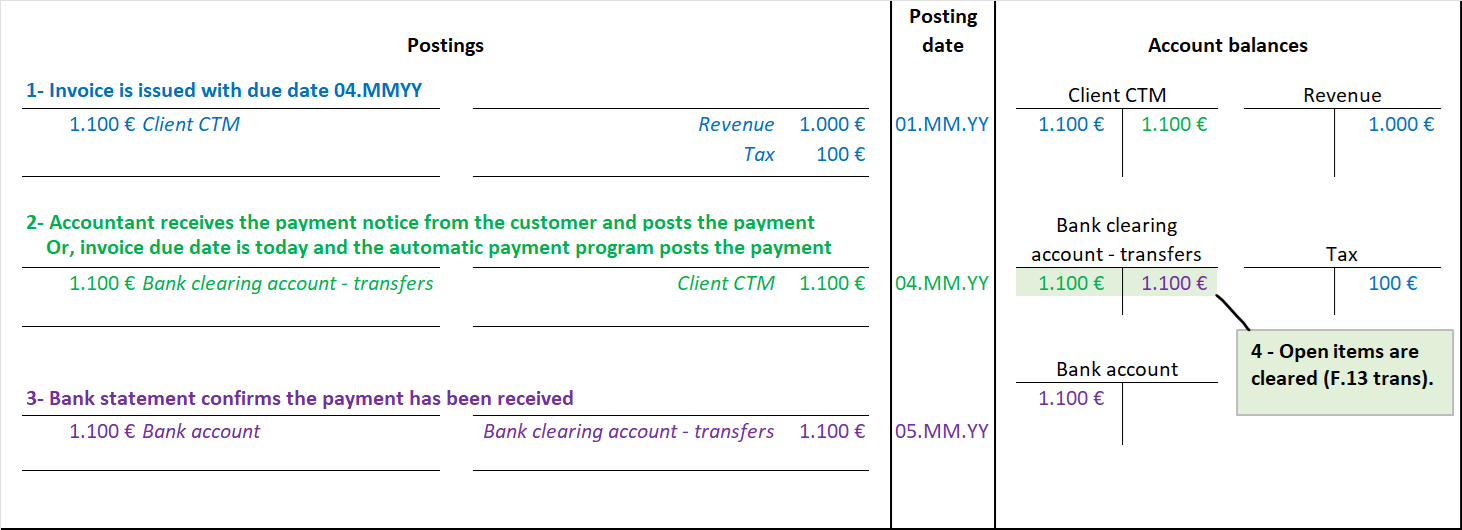

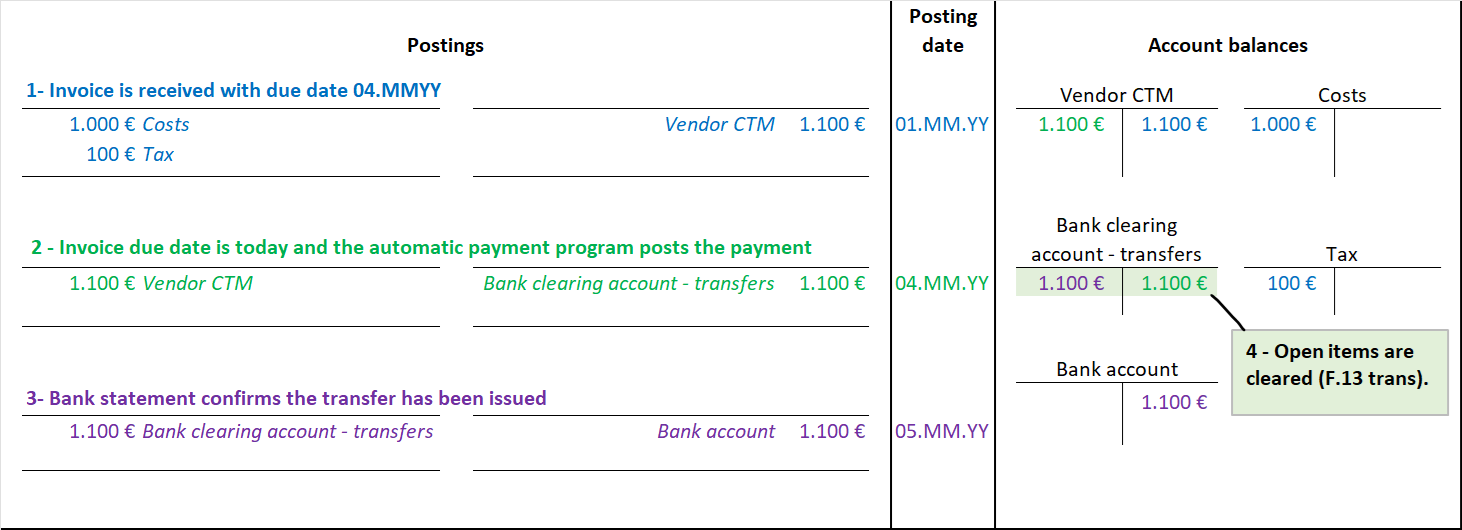

Therefore, the G/L bank clearing accounts will have two postings representing the same payment but with different sign (debit/credit), one posted by the business transaction, and the other by the bank statement. As a result, both postings can be cleared and this is what reconciliation pursues.

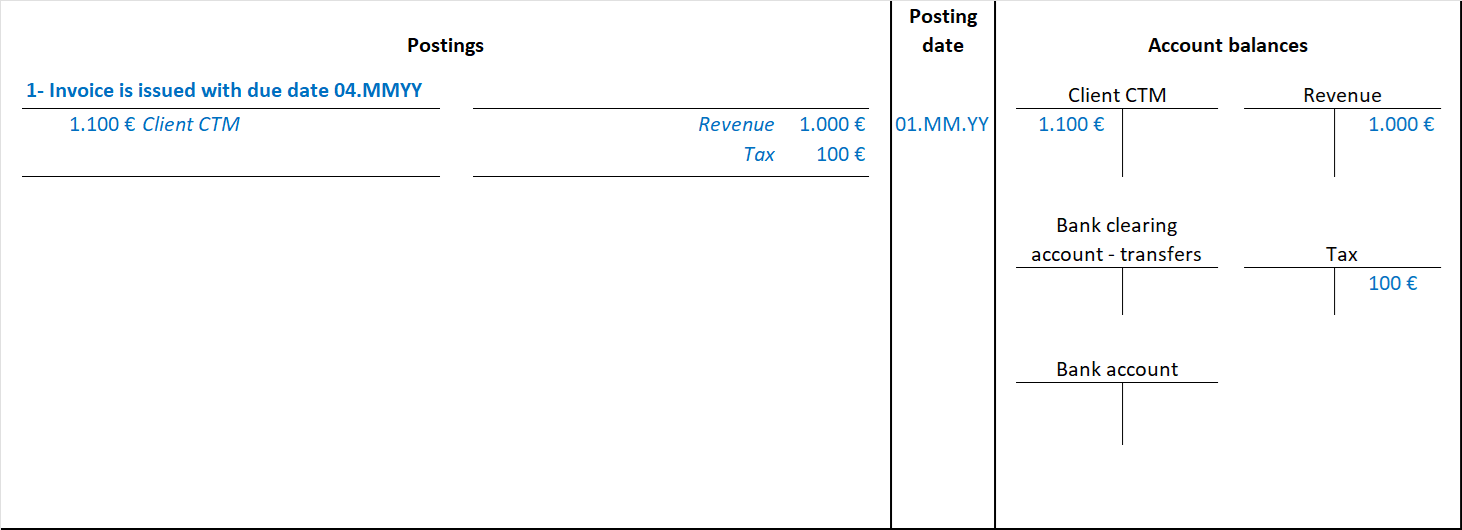

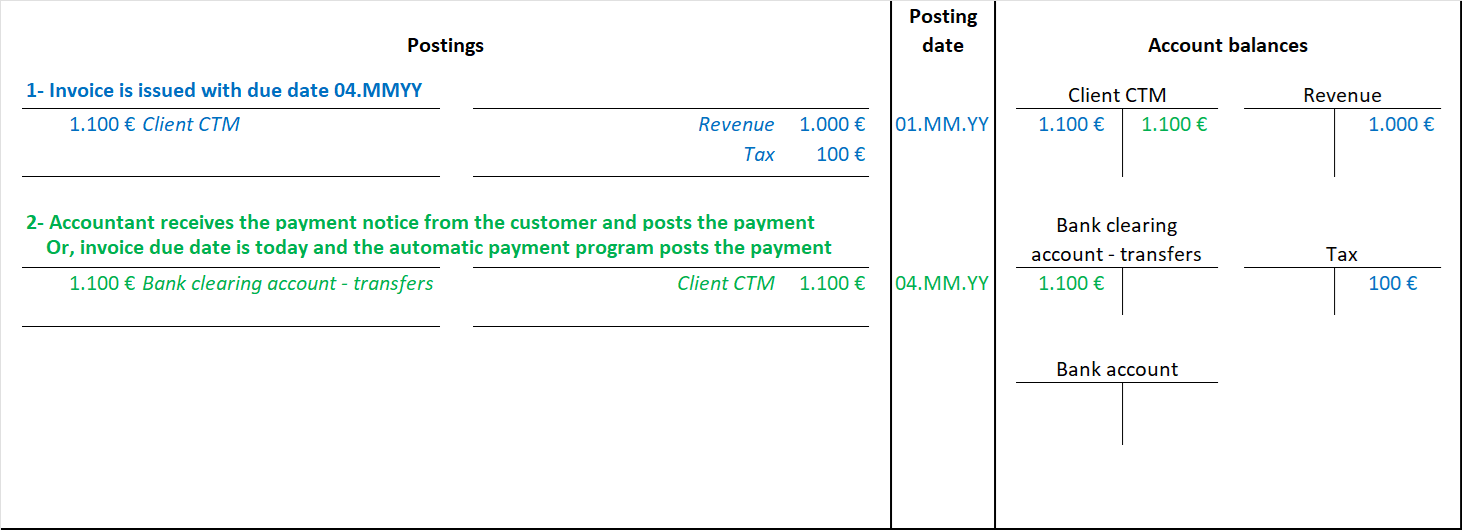

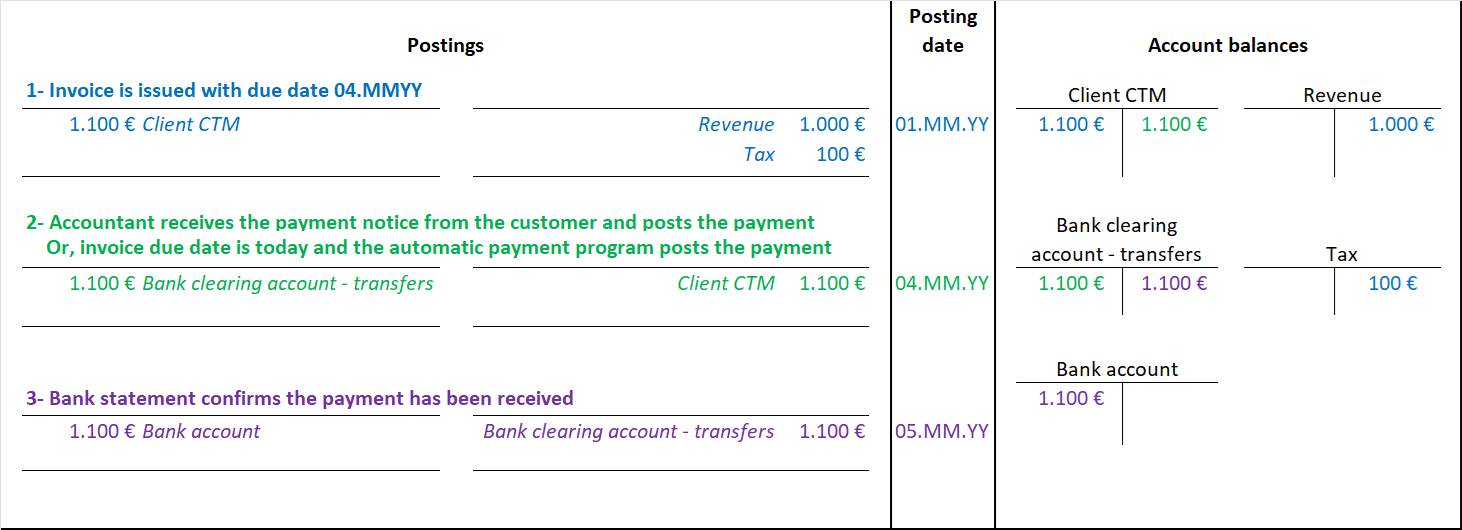

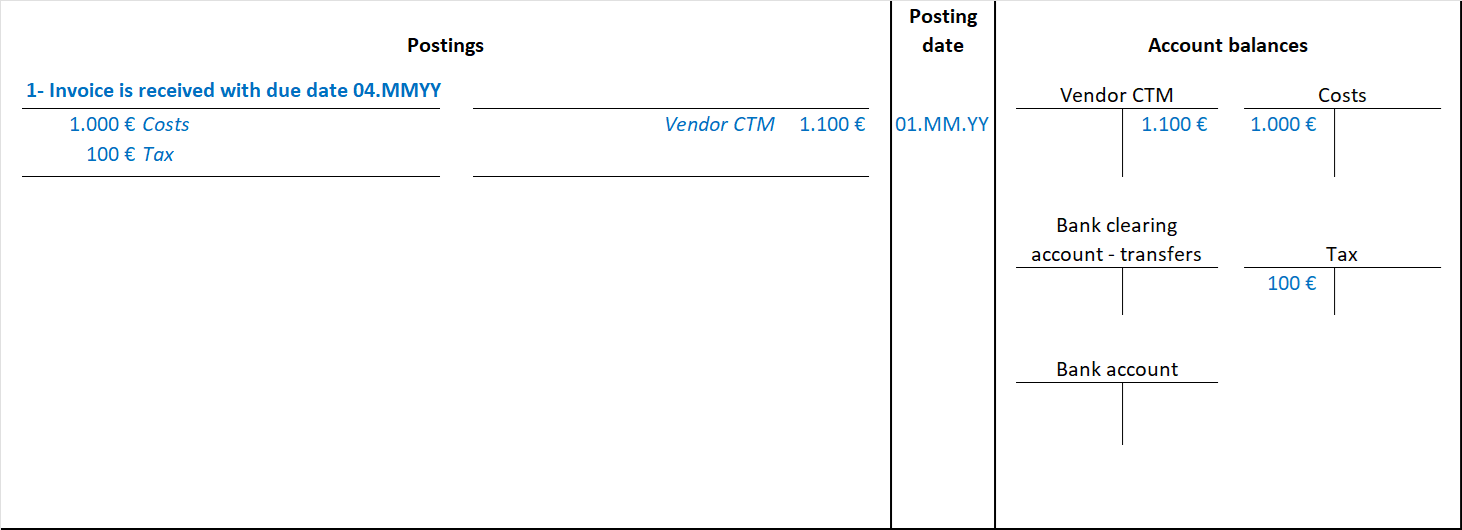

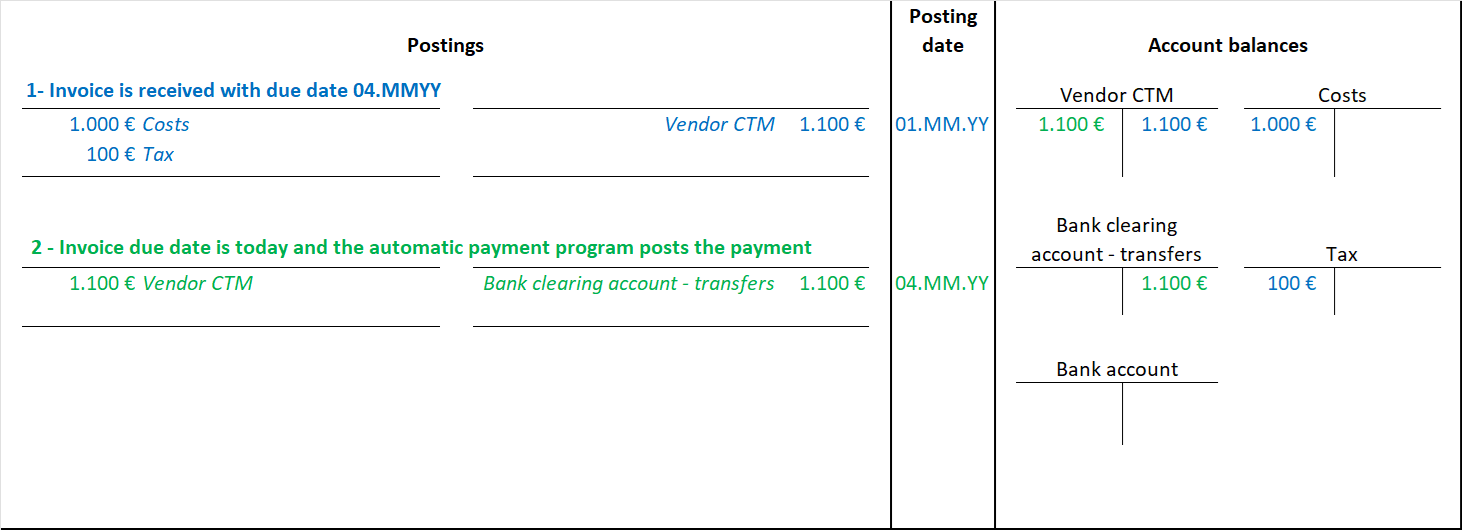

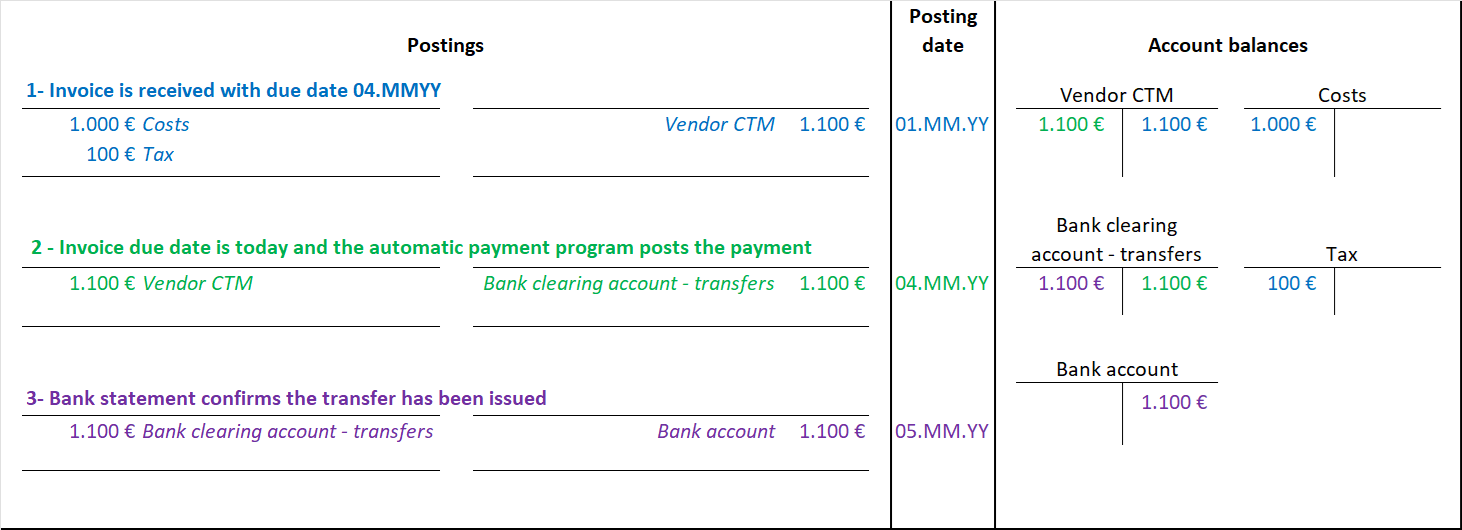

For a better understanding let’s see the postings for an incoming payment received in a company bank account, starting from the invoice issued to the customer:

3. How to deal with balance differences #

When a bank statement item is posted in one of these clearing accounts and then can’t be cleared, this is probably a balance difference that should be analyzed by the accounting department in order to find the reason and then apply the solution.

When the problem is that a bank statement item could not be posted, you will have to run the post-processing transaction to find the reason and post the item. For instance, there could be some new type of items that you don’t have in the EBS customizing.

When all items are posted, there might be some posting to a bank clearing account that the clearing process can’t find any other posting that matches and therefore can’t be cleared. That could be a missing posting in the cashbook.

After applying the solutions the G/L bank account balance must match the bank statement balance, and all the postings acknowledged by the bank statement that had been posted to the G/L bank clearing accounts must be already cleared.